Blogs › Bounce Back Claims

Bounce Back Claims

The new Bounce Back Loans (BBL) could be the answer for many small businesses. Unlike the CBILS, which are very difficult and time consuming to get, the BBL is very simple and straight forward. There are no cashflow forecasts needed, no credit checks and no long delays before an answer is reached, and funds released.

There are a few things to remember with these loans. Firstly, they are loans that will need to be repaid. Secondly, they are over 6 years but with no repayments for the first year and, thirdly, you can overpay with no fees.

So, the main question, am I eligible.......?

The Scheme is open to most businesses, regardless of turnover, who meet the eligibility criteria, and who were established on or before 1 March 2020. Borrowers are required to declare, amongst other things, that:

- The business is engaged in trading or commercial activity, in the UK, at the date of the application. Additionally, the business was carrying on, on 1 March 2020 and has been adversely affected by coronavirus (COVID-19)

- The business (and any wider group of which it is part) is not already in the process of applying for or has not already received a Bounce Back Loan Scheme facility

- The business (and any wider group of which it is part) has not yet obtained a loan through either the Coronavirus Business Interruption Loan Scheme, the Coronavirus Large Business Interruption Loan Scheme, or the Covid Corporate Financing Facility, unless that loan will be refinanced in full by the Bounce Back Loan Scheme facility

- That the business is a company or limited liability partnership incorporated or established in the UK, or tax resident in the UK

- The business is not a bank, building society, insurance company, public sector organisation, state-funded primary or secondary school, or an individual other than a sole trader or a partner acting on behalf of a partnership

- Whether or not the business was, on 31 December 2019, a “business in difficulty” and does not breach State aid restrictions under the Temporary Framework; and if it was a “business in difficulty” then it must confirm it does not breach de minimis State aid restrictions and will not be used to support export-related activities

- At the time of submitting their loan application, the business is neither in bankruptcy, debt restructuring proceedings, liquidation or similar

- More than 50% of the income of the business (together with that of any member of any group of which it is a part) is derived from its trading activity. This confirmation is not required if the borrower is a charity or a further education college

- They will use the loan only to provide economic benefit to the business, and not for personal purposes. They have understood the costs associated with repayment of the loan and that they are able and intend to complete timely repayments in future

The application form also requires confirmations to be given in relation to losses that may be incurred, impact on credit rating, financial risk to personal assets (other than primary residence and primary personal vehicle), reduced consumer protection provisions, data protection consents and that lenders will not assess affordability. Borrowers are advised that they should seek independent legal advice if they are in any doubt about the consequences of the loan agreement not being regulated by the Financial Services and Markets Act 2000 or the Consumer Credit Act 1974 or any other aspect of taking out a loan.

For some businesses, who self-declare as being a “business in difficulty” on 31 December 2019, there may be restrictions on the amount of finance they are allowed to borrow and what they can do with the loan.

Next, How much can you borrow? You can apply for a loan of between £2,000 and £50,000 and to the value of no more than 25% of your 2019 turnover.

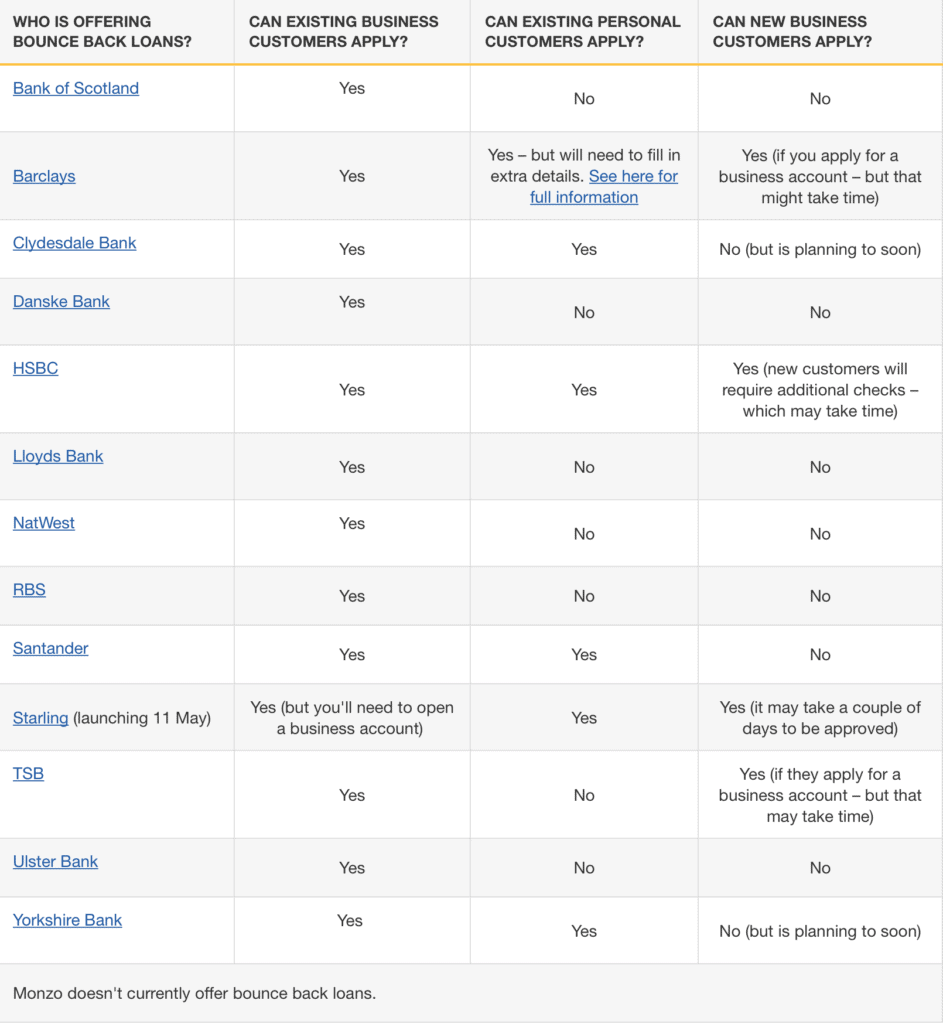

Which Banks are offering this and do you need to be an existing customer?

(Correct at the time of writing)

Having done quite a few of these claims already for clients, DL Accounts can give some advice on different banks and how they work.

Barclays - You apply through your internet banking (they are currently working on applications on the app too). Login and then go to products and services, then business loans. It is straight forward from there.

Lloyds - Lloyds BBL application

HSBC - HSBC BBL application

Natwest - Natwest BBL application

Santander - Santander BBL application

Starling Bank - If you are an existing business customer you will be able to apply online from Monday 11th May 2020 for Ltd companies and Tuesday 12th May for sole traders. If you currently have a personal account you use for business with Starling then login and open a business account. Once opened you will be able to apply. (We will give more info on this on Monday 11th May when it is open).

All of the applications are straight forward to follow so if you're interested in getting a loan to either pay off credit cards at a high rate of interest, purchase that new bit of equipment, cover costs until you are able to trade again or just as a buffer, you will never get a better deal than this one.

Also, if your current bank doesn't offer BBL's or you have been using a personal account and your bank won't help unless its a business account, then we would recommend Starling bank. It's quick and easy to set up (normally the same day), there are no bank charges (other than paying in cash), and the feed into Xero is instant.

If you are a sole trader you will firstly need to set up a personal account. Then, when it has verified you and opened your account, you just login in and request a business account. If you are a Ltd company you can apply straight away for a business bank account.

The application is straight forward and all done online, just follow the instructions. The link to apply for a Starling bank is below.

Updated criteria

What you’ll need during the Starling BBLS application process

All applicants will need:

- An activated Starling business bank card

- A verified email address

In addition

Limited companies will need:

- All persons of significant control added to your Starling business account

Sole traders who started trading on or before 5 April 2019 will need:

- Your 2018/2019 Tax return including the SA100 and SA103S/F

- Your 2018/2019 Tax calculation (SA302), which you can find on your government gateway account

Sole traders who started trading between 6th April 2019 and 1 March 2020 will need:

- Your Unique Tax Reference (UTR) number

- One of the following:

- Your VAT number if you are VAT registered or

- Your 2019/2020 tax return. We know this is earlier than you would normally do your tax return, but it will help us verify your business

Apply for a Starling Bank account here

If you would like any help with these at all, please feel free to get in touch.

Remember to stay positive - we will get through this and those businesses that adapt and create new ways of trading will thrive!

All the best

The DL Accounts Team